The two most significant communications topics among policy geeks these days are net neutrality (NN) and the Universal Service Fund's reform. Both issues are generally discussed inside the beltway as separate and discrete items only affecting telecommunications providers, whereas they are more expansive and interrelated.

Net neutrality, a term coined in 2003 by Tim Wu, was envisioned with the premise that last-mile internet providers were gatekeepers that could act in an anti-competitive manner when doing business with the platform companies. The argument went something like this - because the former telephone companies could make life more expensive and complicated for the platform companies, the phone companies needed the government to oversee their business interactions with companies like Google, Facebook, Netflix, Amazon and others.

To make a long story shorter than it would otherwise be, the FCC instituted new regulations called Net Neutrality laws. Courts struck them down. The FCC reinstated them. The phone companies appealed and the courts upheld the FCC’s rules until a new FCC chairman stepped in and eliminated the new rules, again.

From the time that former FCC Chairman Julius Genachowski passed NN as the official rules in the United States, Google’s worth went from $385 billion in December 2010 to $1.36 trillion (1,360 billion) and they now control 95% of the mobile ad markets, 63% of the browser market; it has become the biggest email provider, and has 50% of the maps market. Amazon’s value went from $59 billion to $1.56 trillion (1,557 billion) and dominates the e-commerce and cloud computing and storage markets. Facebook is worth around $50 billion based on a pre-IPO transaction and is at currently at $738 billion and dominates social media and the associated digital advertising. Their respective founders have become some of the richest men on earth.

Interestingly, you don’t hear about ISPs acting as gatekeepers these days. Perhaps it’s because the gates have shifted to the platforms.

On the edge services market, Google has maintained a search engine market share of more than 85% for the last decade. As we all know, search engines are the gateway to find what you are looking for on the internet. The second choice has a market share of 6%.

While Google likes to claim that competition is only a click away, the reality shows it isn't and they made sure it stayed that way. The European Union imposed a more than $10 billion fine on Google for biasing search results to Google’s own products and services at the expense of its competitors to the point where it was so cumbersome to find a competitor’s product that it was tantamount to blocking.

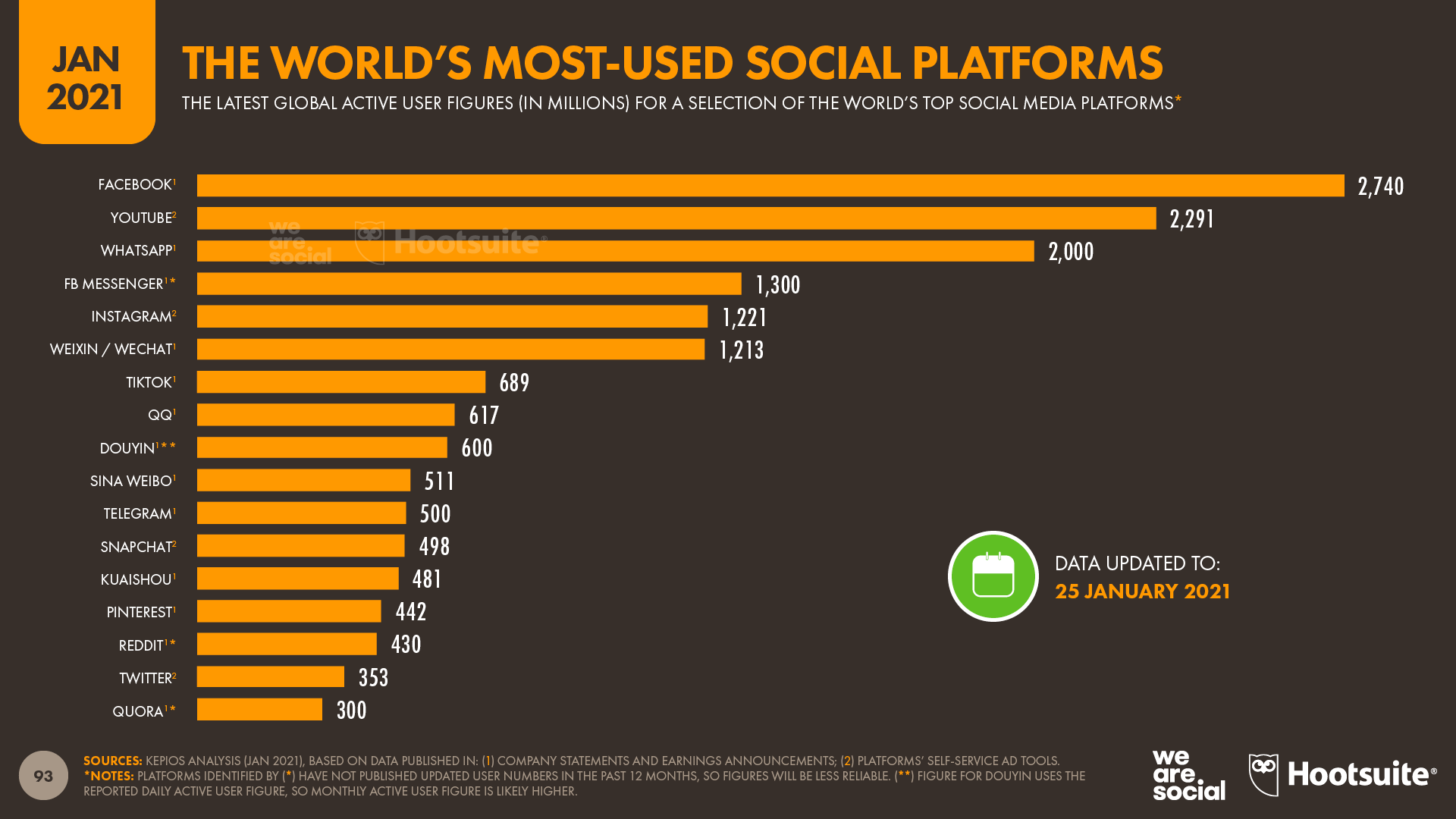

On the social media side, Facebook has also created a juggernaut. Based on the success of Facebook, the company expanded its reach through internal development and the acquisition of competitors. Four of the five most popular social media platforms are now owned by Facebook with a global market share of 45%. If we exclude social media platforms that only provide services in China, that market share increases to 57%.

{kind=link}

Just a few weeks ago, Facebook reacted to an Australian law that required it to share some of the revenue it makes by delivering traffic to news websites with the news providers by cutting all of the links to news sources. Exactly the behavior it warned that ISPs could be doing without NN regulations. The companies that rang the alarm bells about gatekeepers the loudest have become the very gatekeepers they have warned us about.

Market flips

The last few decades have not been as generous for the former phone companies. According to US Telecom, the number of households with gigabit broadband has increased from 6% to 85% in 3.5 years. More importantly, the number of households with a choice of two or more broadband providers increased from 5% in 2018 to 30% in 2020. Eighty-six percent of households have a choice between two or more wired connections. Ninety-seven percent of Americans living in urban areas have a choice between two or more fixed networks. The largest internet service provider in the United States, Comcast, has 23.8% of households in the United States as customers.

And so what is the relevance of these current market statistics? First, they show that America has a nearly insatiable appetite for connecting to the Internet and consuming content. Second, this information shows that the market has flipped. The gatekeepers are now the app stores and operating systems and platforms. These same companies also make multiples of profit from the digital networks ISPs have built, yet only the ISPs are being asked to fund subsidies for low income Americans who can’t afford to connect.

The Universal Service Fund (USF) was designed to bring equal access at comparable rates to all Americans. It succeeded by levying a fee on everyone who used the system through the companies that economically benefitted from connecting people. In the 1930s, this meant that everyone who had a wired telephone paid a fee through their phone bill which funded the USF. As the decades went by, wired phones became less popular in favor of mobile phones and USF got expanded to mobile telephony. As wireless usage increased so did its funding burden.

As the country asks itself how it is going to fund universal broadband, the answer is simple, straight forward and proven over time: Extend the funding source to those who benefit from the system. In 2020, the five largest American telecommunications providers – AT&T, Charter, Comcast, T-Mobile, and Verizon – had net profits of $30.8 billion and if we ignore AT&T’s write down of DirecTV’s value, $46.3 billion. Google’s net profits in 2020 were $41.2 billion and Facebook’s were $29.1 billion for a total of $70.3 billion. When companies benefit so handsomely from an ecosphere, they have an obligation to contribute to its success.

When more Americans are connected with broadband to the internet, Google and Facebook will profit from those connected Americans, so why shouldn’t they help create it?

The internet is an end-to-end ecosphere. People who use the internet do not know who blocked their content. Both edge providers like Facebook and Google and internet service providers are gatekeepers who can block access to content and therefore should be treated the same way when it comes to net neutrality. An internet where only a fraction of the gatekeepers are playing by the rules is still not a fair playing field.

The focus of many net neutrality advocates on Title II is obfuscating the story by deliberately excluding edge providers from the cure of the ills that both can inflict. The calculation is that if ISPs are slapped with net neutrality, the pressure on edge providers to also comply with net neutrality will go away. This might be the case in the United States, but the European Union has shown its willingness and ability to punish net neutrality violations of no blocking (like Facebook’s Australian conduct), no throttling (like Google’s conduct of relegating competitor’s search results into the oblivion of distant search result pages) and maybe even of no paid prioritization (where companies are basically forced to buy the search result of their own company in order to prevent searches being presented with the products of their competitors as their first search result.)

The one neutral internet from edge to core concept extends then to also how we fund the basic equality of access to the internet. Those who benefit from internet access, directly or indirectly, should also fairly contribute to make it accessible to all, regardless of where they live, how much money they make, or what race they are. Only a fully neutral internet where both internet service providers and internet companies are playing by the same rules is truly fair. Anything else is just a distortion of the competitive marketplace favoring one set of companies over another set of companies. The innocence of not doing any evil has unfortunately passed.

Roger Entner is the founder and analyst at Recon Analytics. He received an honorary doctor of science degree from Heriot-Watt University. Recon Analytics specializes in fact-based research and the analysis of disparate data sources to provide unprecedented insights into the world of telecommunications. Follow Roger on Twitter @rogerentner and catch him on The Week with Roger podcast.

"Industry Voices" are opinion columns written by outside contributors—often industry experts or analysts—who are invited to the conversation by Fierce staff. They do not represent the opinions of Fierce.