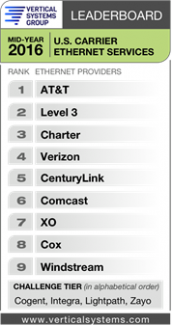

Charter Communications has taken over the third place in the U.S. Ethernet race, edging out Verizon in terms of port share. The jump reflects the gains it made from its acquisitions of Time Warner Cable and Bright House Communications.

The cable MSO debuted on Vertical Systems Group’s Mid-Year 2016 U.S. Carrier Ethernet Leaderboard, a report that ranks Ethernet service providers based on retail port share.

“Clearly, it’s a big move up on the Leaderboard because Charter never retained a spot on the Leaderboard before,” said Rosemary Cochran, principal of VSG, in an interview with FierceTelecom. “Time Warner Cable was previously ranked fifth on the Leaderboard and the combined entities pushed them up over Verizon to start at number three so it’s a major move.”

“Clearly, it’s a big move up on the Leaderboard because Charter never retained a spot on the Leaderboard before,” said Rosemary Cochran, principal of VSG, in an interview with FierceTelecom. “Time Warner Cable was previously ranked fifth on the Leaderboard and the combined entities pushed them up over Verizon to start at number three so it’s a major move.”

By making these acquisitions, Charter immediately gained a larger fiber and hybrid fiber coax footprint to target more small, medium and large businesses with Ethernet services.

With the Time Warner Cable acquisition, Charter gained 150,000 miles of fiber and 75,000 on-net buildings. In addition to its own network, TWC has established 130 E-NNI (external network-to-network interface) agreements with 25 other service providers. This allows Charter to potentially reach into larger business accounts in more U.S. markets.

Meanwhile, the Bright House acquisition gave Charter greater scale across number of key vertical industry segments such as healthcare, hospitality, government and education and a broader Ethernet footprint with an additional 18,000 miles of fiber.

Cochran said that now that Charter has completed these acquisitions, the MSO has to integrate all of the assets under the common Spectrum Business brand.

“These acquisitions give them a much broader network than they had with a coast to coast presence,” Cochran said. “They are looking at putting all of those pieces together, which is everything from the organizational structure, services, and billing.”

Evidence of Charter’s ascension in the business market was also seen in the cable MSO’s second quarter results. For the quarter, Charter reported that SMB and enterprise primary service units (PSUs) jumped. SMB PSU increased by 82,000. In the medium and large business market, enterprise PSUs rose 22 percent, ending the quarter with a total of 90 customers.

What also affected Verizon's ranking was the sale of its wireline properties in California, Florida and Texas to Frontier, a transaction that left the telco with a wireline footprint largely relegated to the East Coast.

“In addition to Charter moving up, Verizon sold off their wireline assets to Frontier and that impacted their numbers,” Cochran said.

However, Verizon’s pending acquisition of XO’s fiber network, which took the seventh place ranking on the Leaderboard, could enable the telco to take back Ethernet share. Upon completing this acquisition following the FCC’s review, Verizon will gain a set of metro networks in 40 major U.S. markets with over 4,000 on-net buildings and 1.2 million fiber miles. The service provider's intercity network also spans 20,000 route miles connecting 85 cities.

“The acquisition of the XO fiber assets is still pending,” Cochran said. “It is possible that deal could be completed by the end of the year, but in terms of the impact we’d have to see what’s left and how we count the ports that are attributed to that.”

The research group noted that from an overall Ethernet competitive market standpoint, 60 percent of new connections were delivered by CLECs and cable MSOs during the first half of 2016. For the full year, the U.S. Carrier Ethernet services grew at a 17 percent annualized growth rate.

“There’s definitely a competitive balance and it’s been changing,” Cochran said. “When you look at where the new business is coming from you have ILECs, CLECs and cable MSOs all represented on the Leaderboard, but in terms of the first half of the year we’re talking about a substantial amount of CLEC and cable MSOs.”

Regardless of the growth, Cochran said that all service provider groups are seeing Ethernet pricing pressures.

“Pricing is stabilizing, but it is a fact that there have been very aggressive Ethernet prices due to competition,” Cochran said. “We were seeing double digit pricing declines, but now it is single digit declines.”

Cochran added that pricing is related the services and speed offerings.

“Pricing depends on what services are offered and what higher speeds are available, particularly if you’re looking at very high speed applications that require low latency,” Cochran said. “There’s not as much competition for low latency services as there is for metro services so there’s a difference in terms of geography, application and speeds.”

For more:

- see the release

Related articles:

VSG: Charter's pending TWC deal could shake up Ethernet services market

Charter’s TWC, Bright House acquisitions increases medium-sized business customer visibility

Charter to focus overbuild strategy on telco competition

Charter's Rutledge says enterprise market penetration is low, but growth prospects are good

VSG: Level 3's tw telecom acquisition helps it surpass Verizon in Ethernet race